FHLB Reform in 5 minutes

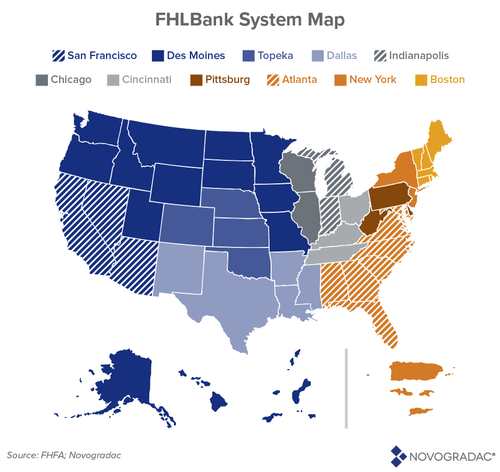

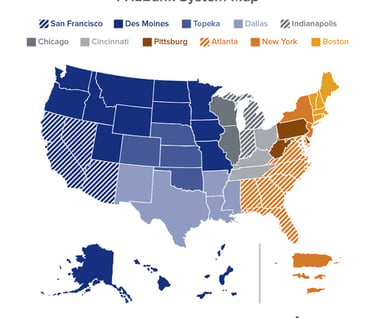

The Federal Home Loan Bank system is a privately owned, tax exempt, government sponsored enterprise with $1.6 Trillion in assets. It consists of eleven FHLBanks owned cooperatively by member banks, credit unions, insurance companies and community development institutions.

Why do FHLBs need reform?

Created by Congress in 1932 to serve as a catalyst for housing finance; the FHLBanks now have almost no direct impact on mortgage finance, give only the statutory minimum of 10% of their net income to support affordable housing, and do very little to support community development.

Why is now the time for a coalition?

The FHFA has launched a strategic review of the Federal Home Loan Banking System. That review, consisting of 19 field hearings, two rounds of written comments and dozens of listening sessions, will result in a report likely to be released in September 2023.

The FHFA’s review thus far has been dominated by the owners of the FHLBanks, with much less input from the general public.

Principles: CFR experts and coalition members will review the report with the following principles for reform in mind:

An equitable balance between the private benefits enjoyed by members of FHLBs (low-cost funding and dividends) and the public benefits of their operations.

Public benefits that include new and existing approaches to funding of sustainable affordable housing, community development, and small businesses lending.

Greater transparency for member regulators, the markets, and the public with timely data on terms and uses of advances and each FHLBank’s affordable housing and economic development activities.

Executive compensation that reflects the public/private nature of the enterprise.

Why does this matter to me?

25:1

That’s the ratio* of the taxpayer subsidy of the FHLBs to every $1 of public benefit the FHLBs deliver. CFR maintains that this is not a good deal for the taxpayers.

Effective reform is likely to be a years-long project. It is important that the massive FHLB system's resources are balanced by a thoughtful voice speaking on behalf of the public interest.

How can I take action?

We are hopeful that the FHFA’s centennial review of the FHLBs in September 2023 will begin the process of correcting inequities in the system. CFR needs experts across perspectives, as well as citizen participation acorss the U.S., to ensure that reforms are balanced and meet the needs of the American people -- not just banks and FHLBs.

By joining CFR, you can have a voice in the reform process, and we will keep you informed on action items, advocacy opportunities, and new developments around FHLB reform. Please get in touch!

*25 to 1 is It is the approximate annual subsidy of the FHLBs ($9.3 billion) divided by the anticipated AHP assessment for ’23.